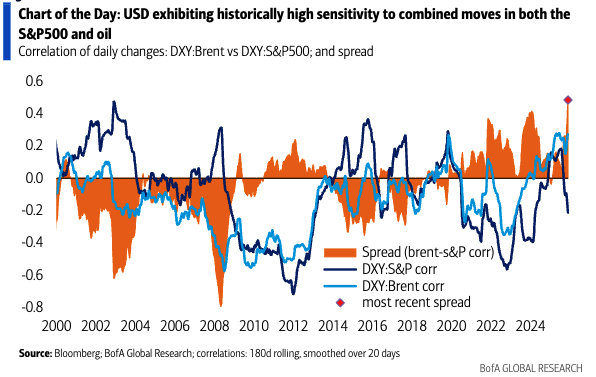

Institutional Insights: BofA Navigating FX In The 'HoneyBadger' Market

## FX / macro takeaway

The core message here is that the post-ceasefire USD selloff may have done the easy part already. Since the ceasefire announcement, DXY has largely round-tripped back into its prior range as markets leaned into the recovery in risk appetite, led by US equities pushing back toward all-time highs. In other words, FX has treated the ceasefire less as a durable macro turning point and more as a cue to unwind the initial war-risk premium. But that reaction may be too neat. While markets seem comfortable with the idea that the US wants to avoid a ground war and avoid compounding inflation risks, that does not automatically imply a rapid normalization in global energy supply, which remains the real macro problem.

That is why the cleaner takeaway now is more two-way USD/G10 risk rather than another straight line lower in the dollar. Oil remains elevated, and even if the most extreme post-war moves have moderated, the energy shock is still sticky enough to tighten financial conditions and worsen downside growth risks — especially outside the US. On relative terms, the US looks more insulated than other developed markets, and that matters for FX. So while the first leg of the post-ceasefire adjustment was a one-way USD depreciation/risk-on recovery, the next phase is more likely to be messier, with the dollar supported by relative growth resilience if hard data begin to reflect the shock more clearly.

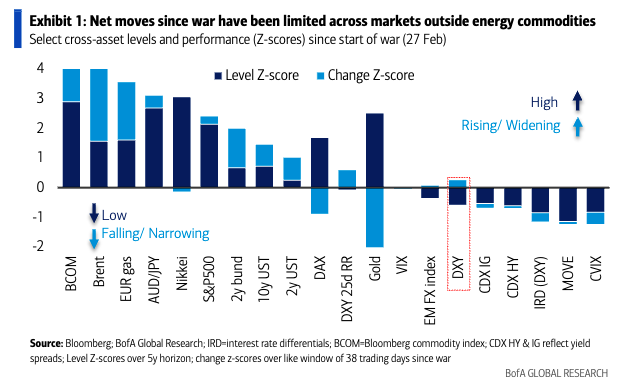

## Cross-asset framing

In broad terms, the market is sending a somewhat inconsistent but understandable signal set:

- Commodities: oil remains elevated and sticky; gold has not behaved like a clean inflation / risk hedge, held back by higher yields and profit-taking.

- Rates: yields are still higher on net, reflecting the view that central banks cannot easily ignore a supply-driven inflation shock.

- Equities: the rebound has been led by the US, and if US equities continue to outperform global peers, that could limit further USD downside.

- Credit: spreads remain relatively calm, suggesting markets are still not pricing a major growth accident.

- FX: the return of risk appetite has pulled the USD back into its range, while crosses like AUD/JPY have outperformed as classic risk-on expressions.

- Vol: FX volatility keeps compressing, which is helping EM recover and reinforcing broader cross-asset calm.

The big unresolved issue is timing:

> When do markets start to care again?

Probably when the hard data begin to show the economic drag from higher energy costs and tighter monetary conditions. Until then, markets can continue to behave as though the worst geopolitical tail risk has passed. But if growth forecasts keep shifting in a way that favors the US over other DMs, then the dollar is unlikely to simply keep falling. The better framing from here is:

> The clean post-ceasefire USD downside is probably behind us; the next move is more likely a choppier, two-way dollar market driven by relative growth and oil persistence.

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 69% and 73% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.

Patrick has been involved in the financial markets for well over a decade as a self-educated professional trader and money manager. Flitting between the roles of market commentator, analyst and mentor, Patrick has improved the technical skills and psychological stance of literally hundreds of traders – coaching them to become savvy market operators!